The City of Yes legislation is, perhaps, the most positive and important piece of legislation passed in many years. It is crystal clear that incentivizing the creation of more housing supply is the solution to New York City’s housing crisis. During the pandemic, vacancy in Manhattan rose significantly, which is the equivalent of an increase in supply. As a result, residential rents dropped by 30%. There has not been a housing policy implemented anywhere in the United States that resulted in rents going down by even 10%. We need new supply and City of Yes will make it a bit easier for developers to create that new supply.

Here is an explanation of some of the component parts of the City of Yes legislation:

Universal Affordability Preference (UAP)

The UAP program (which replaces the former Voluntary Inclusionary Housing program) introduces a density bonus available in R6-R12 districts citywide for developments that provide permanently affordable housing. Developers can increase floor area by up to 20% and gain height increases, provided that a portion of the units meet affordability requirements. The bonus residential FAR must be allocated entirely to affordable units, which may seem onerous until you consider that providing affordable units is the key to qualifying for the 485x tax abatement.

For example, suppose you're developing a new building in an R8B district. Before City of Yes (CoY), your maximum residential FAR was 4.0, and your maximum building height was 85 feet. If you sought the 485x abatement, you would have been required to make 20% of the building affordable, resulting in 3.2 FAR for market-rate units and 0.8 FAR for affordable units. With the UAP program, you gain an increased FAR of 4.8 and a new maximum building height of 95 feet. This allows for 3.84 FAR market-rate and 0.96 FAR affordable, demonstrating how the 485x and UAP programs work seamlessly together.

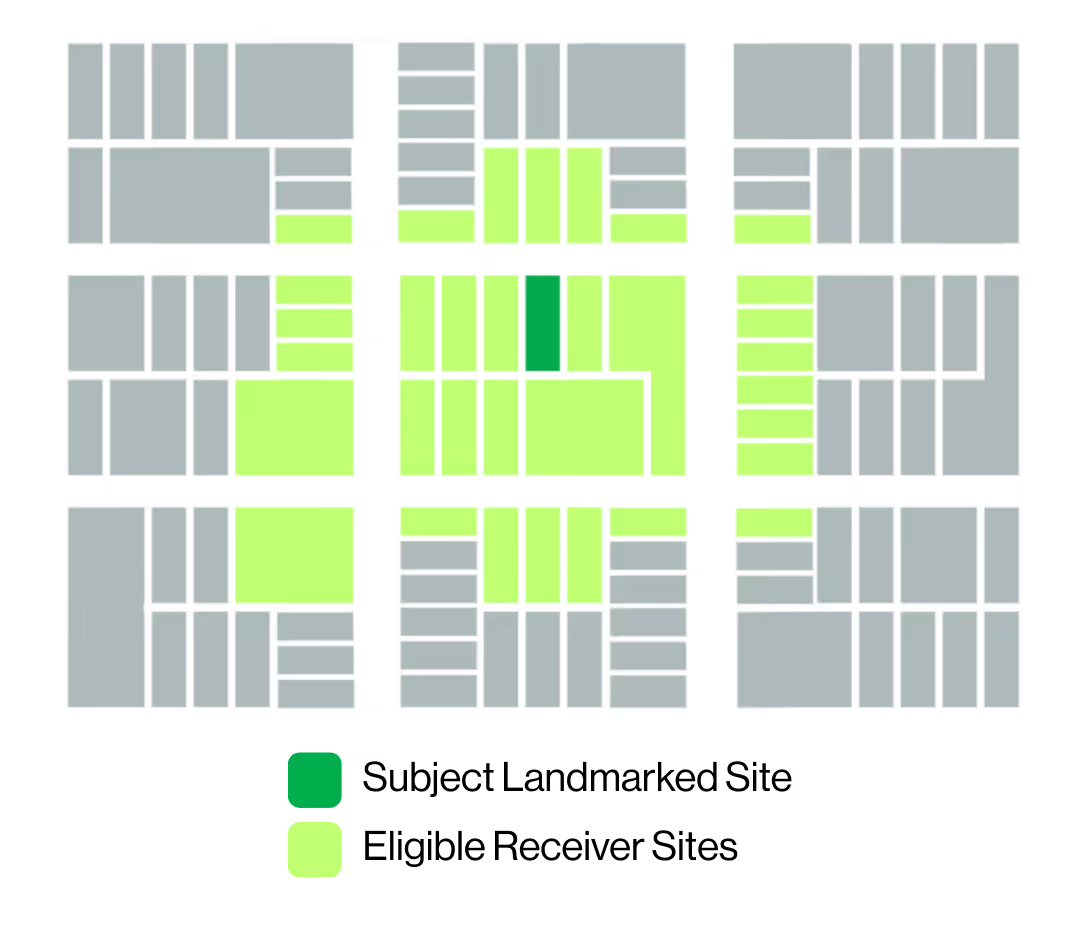

Relaxed and Streamlined Transfers of Floor Area from Landmarked Sites

Until now, individual landmarks have only been able to transfer their unused floor area to adjacent sites, sites directly across the street, or sites directly across the corner. Additionally, any bulk modifications required going through the full ULURP process, which explains why such transfers have not been as frequent as one might suspect. All of that changes with City of Yes for Housing Opportunity (COYHO).

First, landmarks can now transfer floor area anywhere on their block, to properties on blockfronts across the street from their block (north, south, east or west), or to properties diagonally across to the corner property only. Read further down in this newsletter for a more complete explanation. This update fundamentally transforms the market for landmark development rights as most landmarks now have significantly more sites they can transfer their air-rights to, while developers have more options from which to potentially acquire air-rights.

Second, as long as the bulk can be accommodated as-of-right, the transfer can now be done by "certification"—no ULURP, no City Council approval, no two-year drawn-out process. This is a game changer. Do not overlook it. There are caps on the magnitude of increase the receiving site can achieve.

Creation of R11 and R12 Districts

You might have noticed that when we were discussing UAP (above), we mentioned R11 and R12 districts. These new districts are now officially part of the Zoning Resolution, and they are significant. R11 and R12 are high-density districts (expect them to be mapped in Manhattan and central business districts in the outer boroughs) that allow residential FARs of up to 15.0 and 18.0, respectively, provided affordable housing is included.

For now, these districts are established and they will require separate rezonings to be mapped. However, we already know about the first planned rezoning: the Midtown South Mixed-Use Plan, which proposes to map both R11 and R12 districts.

Midtown South Rezoning will turn the Garment Center into one of the hottest residential neighborhoods in the city! Yes, you heard it here first.

Expanded Residential Conversion Eligibility

Here’s one we’ve been discussing a lot this year: COYHO significantly expands the eligibility criteria for converting non-residential buildings into housing. Previously, the rule was limited to buildings constructed before 1961 (or 1977 in Lower Manhattan). The new rule extends the cutoff to 1991 and broadens the geography to include almost the entire city.

This change makes an entire generation of non-residential buildings (constructed between 1961 and 1991) eligible under the zoning’s conversion rules. And let’s face it—many of these buildings could use a lifeline right about now. With almost 90 million square feet of vacant office space (particularly in Class B & C assets), and a desperate need for housing, this new legislation should produce a ton of activity.

Sliver Law Reforms

The “sliver law,” which has restricted building heights on narrow lots for decades, has been eliminated for projects utilizing Quality Housing regulations (those with defined height and setback requirements). This change significantly enhances the development potential of certain small sites (“infill” sites) in high-density neighborhoods.

There have been some districts in Midtown that did not have Sliver Law prohibitions, but virtually every other neighborhood in Manhattan did. This will change the nature of the boutique development business.

Increased Height for Large Sites

Here’s one more accretive aspect that didn’t get much attention during the public review process. Take a look at the new ZR Section 23-434 (it’s in here, which is all we have for now), which allows for taller buildings on “eligible” sites. This addresses a longstanding issue with the city’s contextual zoning rules: their lack of nuance, particularly for larger sites. Finally, there’s some relief.

I’ll leave it to our zoning and architecture professionals to fully unpack the ramifications, but my take is that this change is very consequential for larger sites in contextual districts. One example: in R8 districts, under the Quality Housing rules, the maximum height has been 135 feet. Per the new Section 23-434, on eligible larger sites, that height increases to 215 feet—or up to 255 feet if UAP is included. That’s no small difference!